LIC Annuities: Marketing gimmick at its best

Even with "guaranteed double digit rates" offered by these schemes, why do they not work

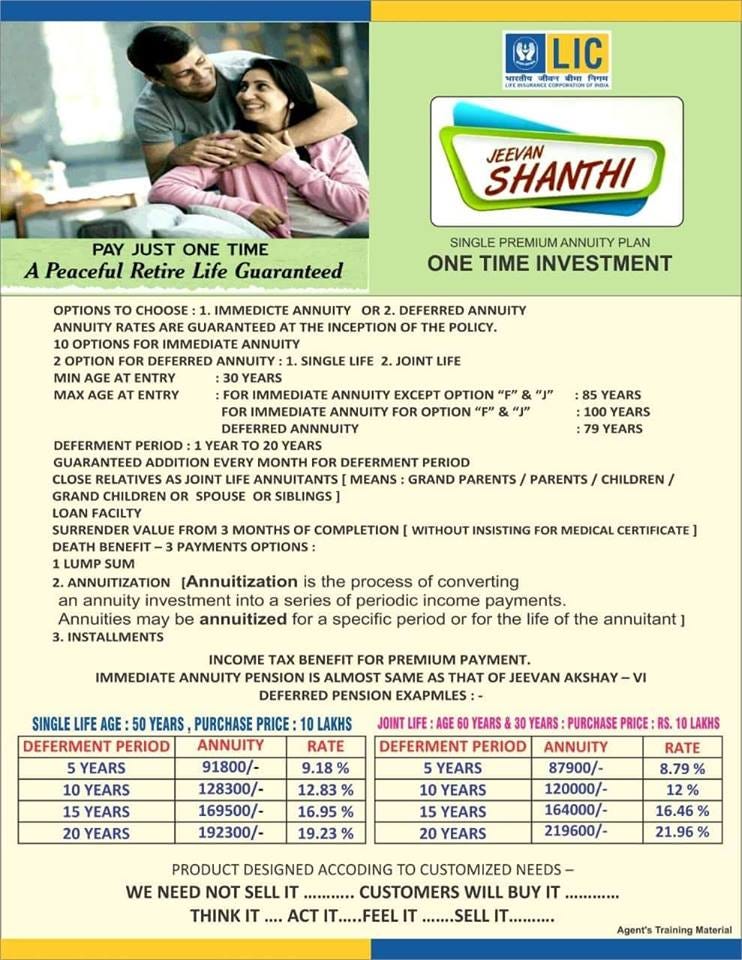

LIC Annuity Schemes.

We all know someone who invests in these plans, so as to earn a consistent annuity income post retirement. But how effective are these schemes for real ?

What are Annuity Schemes?

An annuity scheme basically is a plan where you prepay a lumpsum amount and in return, the scheme offers to pay you a fixed amount each year (or each month or so on), for the rest of your life, at the end of a deferment period.

In addition, there are also further payouts such as a death benefit at the end of your life, which on an average is about 110% of your original investment.

A scheme such as this is supposed to be great for the folks heading into retirement.

Sounds pretty amazing, doesn’t it?

Here’s an advertisement I found for one such scheme.

Imagine earning guaranteed rates up to 16% and 19% per year on your investment AND getting back 110% of your investment at the end of your life as well.

“When things look too good to be true, they probably are.”

Let us see what this is all about.

1) Deferment Period: Since our entire country has never really consider personal finance as an important criteria growing up, we do not factor in the impact of deferment years on our total returns.

Deferment Period is the number of years wherein you would not be earning any returns at all. Nada. No cash inflows at all.

“Yeah, but that is like 5 years only”

The above scheme is for people who are of at least 50 years age. If you Google the average life expectancy in India, it is 69.16 years. Let’s call it 70 years. The minimum deferment is for 5 years. So, over the last 20 years of your life where you would need the funds, you would not receive a penny for 5 out of those 20 years.

2) Rates: To better understand the impact of deferment period, let us look at the “Rates” being offered in the scheme.

The rates are expressed as a % of the original investment. Since they will be paid out and not eligible for compounding, it is a fair representation as such.

But.

Now combine the Deferment Period and the Rates offered, and that’s a recipe for disaster.

Debunking Actual Returns:

Based on the 4 plans advertised above, I have calculated the ACTUAL RETURNS which someone investing in the plan would earn.

Assumptions:

(Based on average life expectancy, I have considered the term of the plan up to 70 years, a death benefit of 110% of original investment and a super important assumption that people are still with me at this point)

For anyone who’s new, IRR is the method that factors in the effect of time in receiving and paying out cash (aka deferment period).

Remember how rates mentioned in the ad were increasing from 9% to 12% to 16% to 19%, for longer deferment periods? Well, see how the actual returns actually fall because you delay receiving cashflows ? Personal Finance 101.

Also, these returns are pre-inflation. With inflation in the range of 6%, most of these schemes will actually offer you negative real returns.

Sorry to the suckers who invested in the scheme. The misleading advertisement of the largest life insurance company in India got to you.

If nothing, the only feedback you should consider from this is that: A rupee earned today, is way more valuable than a rupee earned 1 year later.

So get all those cash inflows in 2021 instead of deferring them to 2022.

Wish you a happy new year, folks!