The "Silver" Lining in Silver

The "Silver" Lining in Silver

A dive into the recent rally in the precious metal, and a possible method of pricing the commodity.

Well, as some may have guessed from the title, this is a post about the metal which has been having a party of its own for the last few months. Silver, of course. Let us try to make sense of the kind of price move we have seen in this precious commodity over the past few months.

While this can clearly be considered by many as the kind of post which makes sense in hindsight, I have been toying with the idea of blogging about my investment journey for a while, and I decided to go for it now, since I do have some time on my hands, because of the pandemic.

Now as with any good plot, apart from the protagonist, there are a bunch of supporting actors which make a plot truly amazing. In terms of the play on Silver, these supporting actors, could be the following:

1) The Pandemic

2) The US Fed

3) The Miners

4) Gold

Let's try to dive into this not so intricate plot, via these supporting actors.

1) The Pandemic

Indubitably, this is the event that set the ball rolling for the entire plot.

With the entire world being under a strict lock-down because of the Coronavirus, there was an implied halt on all economic activity around the world as well. This halt would continue for the foreseeable future with no vaccine in sight.

A halt on economic activity implies a slowdown of businesses, pay cuts, job losses, a setback in the stock market and a fear of recession.

With the advantage of writing this a few months later, we can all affirm that it did in fact, happen.

Well, most of it did.

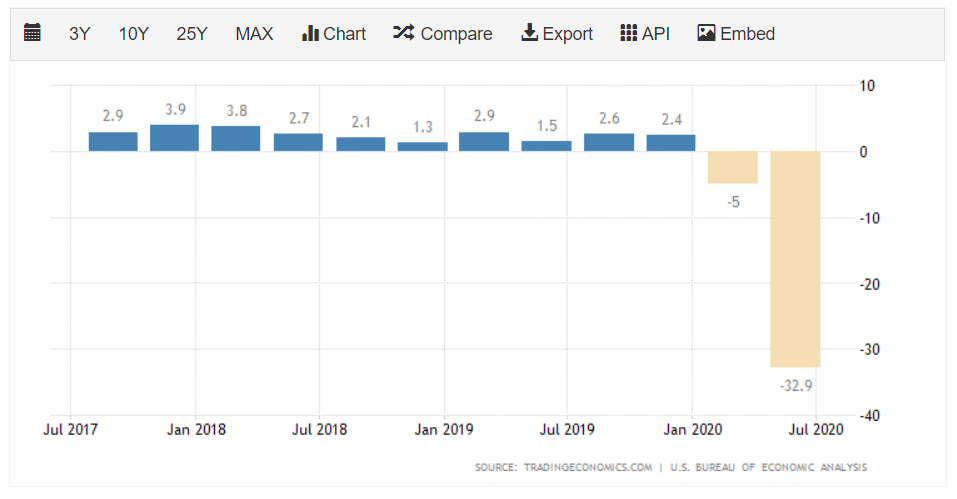

Impact on US GDP Growth Rate:

Impact on US Initial Jobless Claims:

(Remember the Global Financial Crisis of 2008? You see, how tiny the impact of the same was on number of people out of jobs vis-a-vis now?)

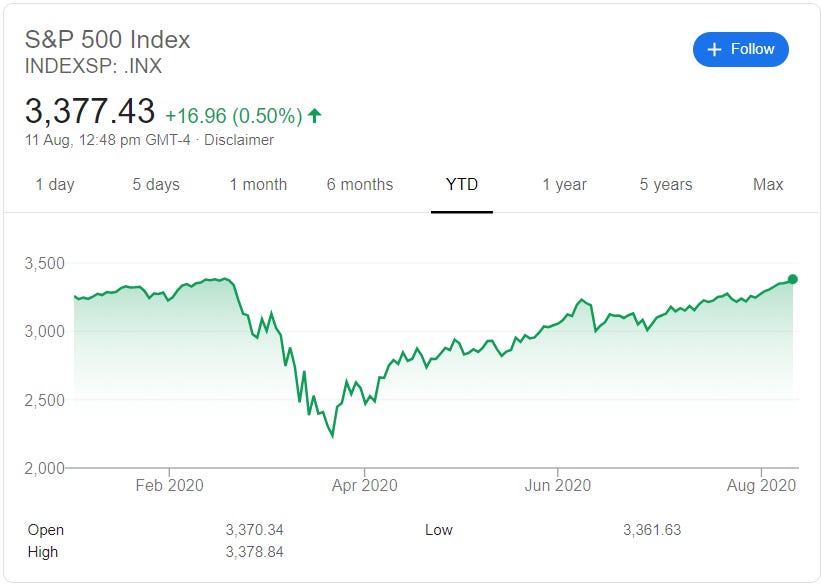

US Stock Market:

Even though this is in hindsight, the stock market performance over the last few months is certainly baffling.

So let us talk about the next supporting actor, who added fuel for the stock market.

The Fed, of course.

2) The US Fed

I have never followed the actions of the US Fed too keenly, because I am a bigger advocate of Austrian economics rather than Keynesian (more on that another time). But, to say that the actions of Fed have been a huge influence, is almost like an understatement.

At a time when cash generation by businesses and households is arduous, the US Fed Chairperson, Jerome Powell, publicly announced that the Fed would do "whatever it takes" to keep funds flowing in the US economic system.

And this of course, gave birth to the infamous money printer memes.

(Not going to lie, feels good to be contributing to the meme community.)

What the US Fed achieved with its plans of printing trillions of dollars and buying not just government bonds, but corporate bonds too (!!!), was free flow of credit to the large corporate world.

Normally, this would work and it would be the end of the story with Silver not even appearing in the picture. But let us not forget about supporting actor 1, the pandemic and the lock-down.

With money flowing to corporate houses, it was not exactly possible for them to boost their spending and manufacturing activity, because there still was no vaccine for the virus and employees would not be working.

But that's the US Fed for you. Which tried to solve a pandemic by throwing money at it.

Now, we're in a situation where there is a slowdown of real output due to reduction in manufacturing activity due to a lock-down and a case of high supply of money in the system. You know what follows with these two ? Inflation.

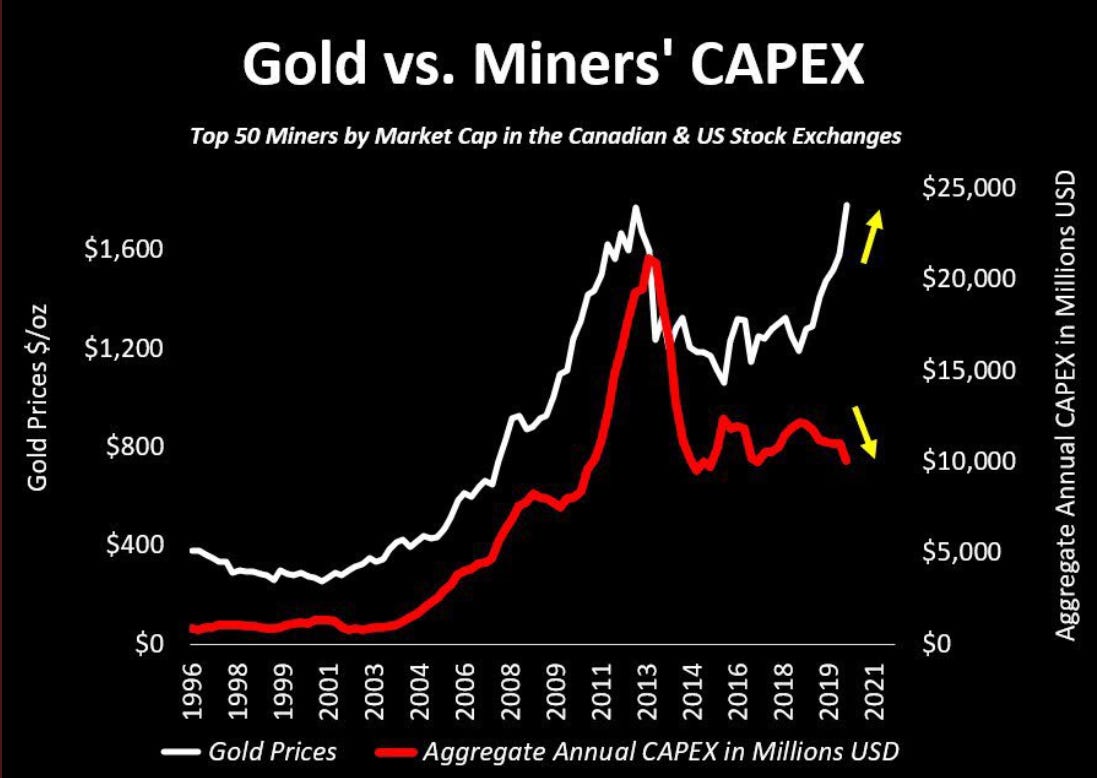

3) The Miners

In case, anyone is unaware about this, inflation basically means that the currency of the country loses its value. In this case, it is due to the excess supply of the same.

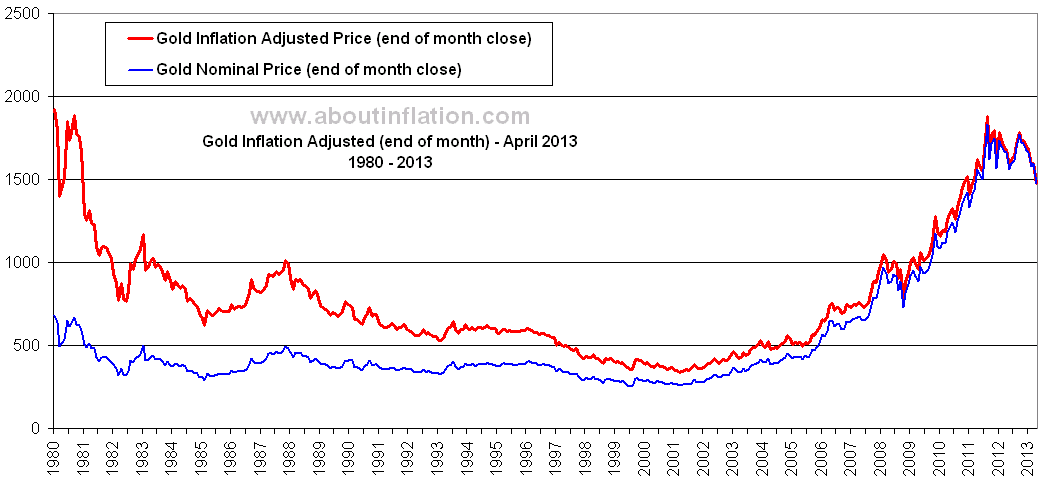

In times of inflation, gold becomes a tool to hedge against inflation, which pushes the gold prices higher.

And who produces this commodity? The miners.

Basing the discussion on the earlier point, there would also be a lower real output of any commodity mined, due to the lock-down.

To make matters worse (well, better, for miners and gold), was the reducing capex spend by mining companies, with Gold prices, already rising.

No capex, obviously means no investment in further infrastructure to mine more gold.

This makes the case all the more bullish for Gold, with an almost finite output, rising Gold prices and inflationary conditions.

4) Gold

While, this may all along have seemed like a post about investing in Gold, the plot twist, like in a M. Night Shyamalan movie, is introduced by our last supporting actor, Gold, itself. Almost, like an antithesis, if you come to think of it.

So what is it about Gold, that makes you want to buy Silver instead of Gold itself.

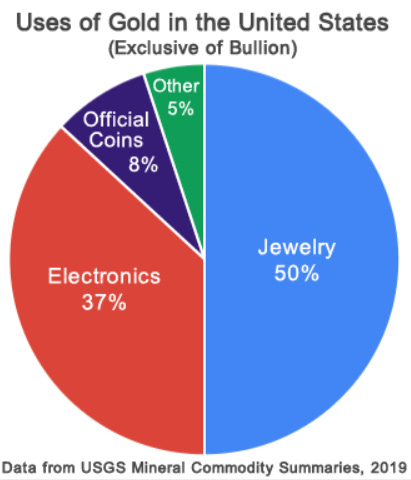

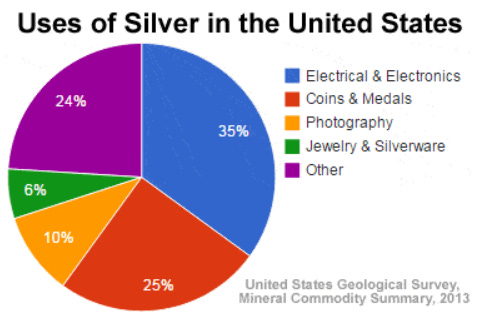

A glaring point of difference between the two metals is the end use application of the metals, themselves, but that isn't exactly the point to focus on in the current time.

Speaking of similarities, is the correlation between the movement of gold and silver prices and how they mirror each other over long term periods.

Since, the price movement of gold and silver is in tandem, why would we even be worried as to which to buy? Wouldn't they both be the same?

I mean, you cannot exactly run a DCF model on commodities, since the assets do not produce cash flows which can be discounted to find a value as on today.

That leaves us with the option of pricing via the relative valuation model.

But the prices of gold and silver should be compared, relative to what? GDP, Market indices, Bitcoin, M2 (Money supply), Debt ?

None.

The simplest indicator which was a screaming buy for Silver was the Gold/ Silver ratio. This ratio basically indicates how much quantity of silver is required, to purchase an equivalent quantity of gold.

Higher the ratio, the more undervalued silver is and lower the ratio, the more undervalued is gold.

As can be seen above, the Gold/ Silver ratio was at an approximate level of 110. That means, 110 ounces of silver was needed to buy just one ounce of gold!

To reaffirm, the above relative valuation, I did dig a little further and found that the long term Gold/ Silver ratio has been in the range of 60 - 70. At 110, it did seem to be at a discount of almost 40% to its "intrinsic value", based on the relative valuation.

Absurd, I know. But it is absurd times, that we are in!

Now, whether Gold is overvalued or Silver is undervalued, was the question.

Since I don't particularly like to engage with too much speculation activity in the derivatives market, I did not think of the idea of shorting Gold and instead purchased some Silver bullion itself (Since there are no silver ETFs available in India, unfortunately).

For someone who would be more interested in trading this view, a "Long-Short" bet with Long Silver contracts and Short Gold contracts would have been an amazing bet since it has the hedging within the asset class, while fundamentally remaining long on the undervalued commodity.

Of course, there may be an element of hindsight bias here, however.

Apart from the above reasons, there are a lot of structural changes such as reserve currency debasement, a regime of lower real rates, etc, which I think would be a great runway for precious metals like Gold and Silver.

At the time of writing this (11 August 2020), Silver has just crashed by a whopping 14% and trading just a tad bit above USD 25/ Oz. I continue to hold the silver bullion I bought at the end of April as well as with the ongoing SIP in Gold ETFs, and would like to add more to my position on declines.

Very insightful! Keep on posting good ideas. Looking forward for more of such!